Trying to navigate the tax world can be confusing when you’re not an expert. As a result, you may overlook valuable tax credits and end up shortchanging yourself. Luckily, using ezTaxReturn and familiarizing yourself with what’s out there can help. In this article, we’ll which tax breaks can save you thousands in taxes.

Earned Income Tax Credit (EITC)

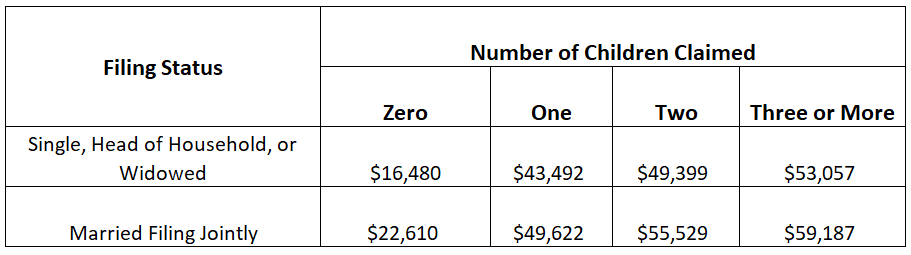

Normally when taxpayers see that their income doesn’t require them to file a return, they do a little happy dance and move on with their lives. However, that’s a bad move because workers earning less than $59,187 may qualify for the Earned Income Tax Credit. Not only can this credit lower your tax bill but it can also put some cash in your hand since it’s refundable. To qualify, you must meet the income requirements based on your filing status and number of dependents. Being childless won’t get you disqualified but your credit will be much lower than if you had kids. For tax year 2022, the earned income and adjusted gross income (AGI) limits are as follows:

Additionally, you cannot earn more than $10,300 in investment income. So how much is the credit worth?

- $560 with no qualifying children

- $3,733 with one qualifying child

- $6,164 with two qualifying children

- $6,935 with three or more qualifying children

Last year, 31 million taxpayers received the EITC but 1 in 5 eligible workers still missed out. Get every penny you deserve by using ezTaxReturn to do your taxes. We make it easy to save hundreds or thousands of dollars in taxes, so you get the biggest possible refund.

Saver’s Credit

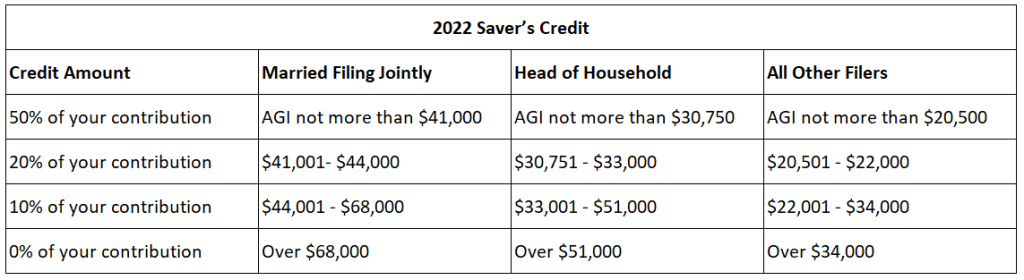

According to the U.S. Census Bureau, 49% of adults aged 55 to 66 have no retirement savings. Even if you’re on a tight budget, start contributing to an IRA or employer-sponsored retirement plan anyway. The IRS rewards taxpayers who save for their future by offering the Saver’s Credit. The credit is worth 10, 20 or 50 percent of your contributions up to $2,000 ($4,000 if married filing jointly). This means a single person can receive a maximum credit of $1,000 and married couples can receive up to $2,000. The exact percentage you’ll receive depends on your adjusted gross income. For an estimate of your potential savings, use the chart below.

Child Tax Credit and Additional Child Tax Credit

According to the CDC, close to 4 million babies are born in the U.S. each year. Whether you’ve recently welcomed a bundle of joy or already have a child under the age of 16, you may qualify for the Child Tax Credit. Each child is worth up to $2,000 in tax savings.

Child and Dependent Care Credit

For many families, childcare is one of the biggest expenses. Luckily, parents can receive up to 35 percent of their expenses back as a Child and Dependent Care Credit, depending on their adjusted gross income. However, there is a limit to how much you can claim. The maximum is $3,000 for one child and $6,000 for two or more children. The IRS also doesn’t just give the money away, you must meet a couple of qualifications. For starters, your child must be under the age of 13 or mentally or physically unable to care for themselves. Second, you cannot claim the credit if either you or your spouse is a stay at home parent. You’ll only qualify if you paid someone to watch the kids while both of you went to work or were on a job interview.

American Opportunity Tax Credit (AOTC)

CollegeBoard reports that students staying home to attend a public four-year college pay an average of $10,950 a year for tuition and fees. That’s a pretty penny especially if parents are footing the bill for multiple kids. To minimize the expense, the IRS offers the AOTC for students who paid for tuition, enrollment fees and textbooks during their first four years of college. The credit can save you up to $2,500 per student and comes with an additional perk. Since it’s partially refundable, you may be able to get up to $1,000 back as a refund. Eligible students must:

- Be working towards a degree or other recognized credential

- Be enrolled at least part-time each semester

- Not claim the credit for more than four years

- Not have a felony drug conviction

Lifetime Learning Credit (LLC)

The Lifetime Learning Credit is another education credit that can save your thousands in taxes. Unlike the AOTC, there’s no limit to the number of years the credit can be claimed. Whether you’re taking undergraduate, graduate or professional degree courses, your expenses may qualify. The LLC is worth up to $2,000 per tax return. To qualify, students must be:

- Enrolled or taking classes at an eligible institution for at least one academic semester

- Working towards your degree, certification or improving your job skills

Please note, you can’t choose both the LLC and AOTC on your taxes, it’s one of the other.